Table Of Content

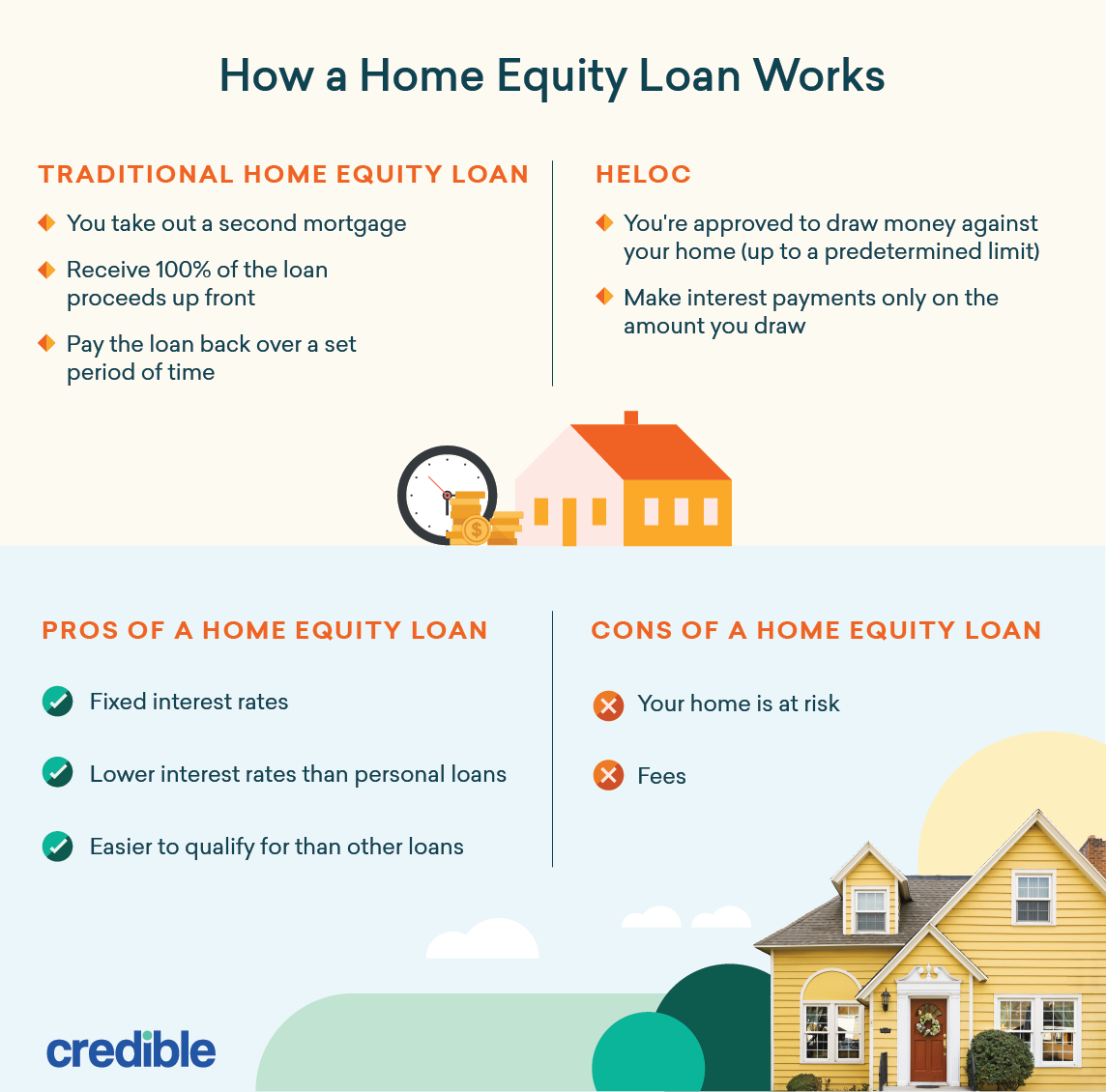

However, if your existing mortgage rate is significantly lower than current refinance rates, you probably won’t want to replace it with a loan that will cost you more in the long run. During the HELOC draw period, you can use and reuse the credit line as many times as you need, as long as you don’t exceed the limit. Many times, you have the advantage of low, interest-only payments during this phase.

Phase 2: The Repayment Period

Talk to a Rocket Mortgage Home Loan Expert to learn more about tapping into your home’s equity. Each time you make a payment on your mortgage, you add to the amount of your home that you own. A cash-out refinance allows you to refinance your current mortgage loan, meaning you replace your existing mortgage. A cash-out refinance replaces your existing mortgage with a new one for a higher amount so you can pocket the difference.

Are home equity loan rates similar to mortgage rates?

But, when done prudently, a home equity loan or HELOC could provide significant financial flexibility at a relatively affordable cost in today's environment. A home equity line of credit (HELOC) can be a good option for construction, home renovations or other expenses that you’ll pay over time. Similar to a credit card, a HELOC lets you borrow as much or as little of your available credit as you want; you don’t have to borrow a lump sum all at once. And HELOC closing costs can be minimal as long as you don’t close your line of credit within 36 months of opening it. It also allows customers who have applied for a loan to follow along with the approval process and upload supporting documents.

Can you refinance a home equity loan?

Be aware that their value estimates are not always accurate, so adjust your estimate as needed considering the current condition of your home. Then divide the current balance of all loans on your property by your current property value estimate to get your current equity percentage in your home. The interest rate on a home equity loan—although higher than that of a first mortgage—is much lower than that of credit cards and other consumer loans. That helps explain why a primary reason that consumers borrow against the value of their homes via a fixed-rate home equity loan is to pay off credit card balances. During this period, you can borrow from your line of credit as needed and make minimum or interest-only payments on the amount you borrow. If you reach your credit limit, you’ll need to repay some of your balance before you can borrow more money.

They are often unsecured, meaning your home isn’t used as collateral, reducing the risk of foreclosure. However, interest rates for personal loans can be higher than home equity loans, as lenders take on more risk. These loans are most beneficial for smaller expenses or debt consolidation and usually have fixed interest rates and a predetermined repayment schedule. A home equity loan is a second mortgage that allows you to use your home’s value as collateral to pull out cash in a lump sum. You can use the money to finance home renovations, consolidate credit card debt or pay for other large expenses. Once you’ve received your loan, you start repaying it right away at a fixed interest rate.

Like a credit card, you have a certain spending limit and when you reach that threshold your credit stops. While HELOCs and home equity loans both allow you to tap into your home equity, the right one for you will depend on your individual circumstances and financial goals. Unfortunately, most of the other factors, such as the timing of the home appraisal and underwriting process, are less in your control. If your financial situation is clear cut, the underwriting phase has a better chance of moving along quickly.

So, you can pay less overall with home equity loans versus a cash-out refinance that charges closing costs on the existing mortgage amount plus the borrowed equity. Many homeowners believe that selling their house is the easiest and most convenient way to get a needed cash influx. However, accessing your home equity can be a smart way to borrow—without having to sell your home, take out expensive personal loans, or rack up credit card debt. A cash-out refinance refers to using your equity to get a new mortgage that's larger than the amount owed on your existing mortgage. Then, you pay off the existing mortgage and use the remaining money as needed.

year term home equity loan rate

The 7.99% starting APR is specifically for its 10-year home equity loan. However, loan terms range from five to 30 years with a minimum amount of $10,000. Additionally,TD’s home equity loans aren’t available in all states.

HELOC And Home Equity Loan Requirements In 2024 - Bankrate.com

HELOC And Home Equity Loan Requirements In 2024.

Posted: Wed, 27 Mar 2024 07:00:00 GMT [source]

Should I Refinance My Mortgage And When?

This type of loan enables a homeowner to borrow up to 85% of their home equity and pay it back in monthly installments over a period of five to 30 years depending on the loan term. While the average credit card interest rate is over 20% and the average personal loan interest rate is over 12%, the average 10-year home equity loan interest rate is just 8.77%. And, the average interest rate on a 15-year home equity loan is slightly lower at 8.76%. For example, the average home equity line of credit (HELOC) interest rate is currently 9.07%, more than a quarter point higher than either home equity loan option. This nearly unmatched flexibility makes home equity borrowing an attractive option if you need to access a large amount of money now at an affordable rate. And rarely do major credit card issuers extend revolving credit limits higher than about $30,000 without the cardholders having stellar credit profiles and high incomes.

But once the repayment period begins, you can’t withdraw from the credit line anymore and must repay the loan balance and interest in full. Depending on your retirement plan, you may be able to borrow against your 401(k). This can be an attractive option as you’re essentially borrowing from yourself, and repayments go back into your account. However, you also lose out on potential investment growth during the loan term.

Joshua Rodriguez is a personal finance and investing writer with a passion for his craft. When he's not working, he enjoys time with his wife, two kids, two dogs and two ducks. As stubborn inflation continues, interest rates may head up in the future.

The credit union also allows you to borrow up to 100% of your CLTV for a first and second home, which is higher than most competitors. Loan TermsThe rate quoted above is good for a 10-year loan term, though you can borrow for terms of five to 30 years. The lower rate also requires automatic withdrawals from a TD Bank checking or savings account. Common uses include debt consolidation, education costs, home improvements and business startup costs. Reach out to three to five lenders and see what kind of home equity loan terms they may be willing to offer you.

In addition, you’ll want to compare annual percentage rates (APRs), which more accurately represent the total cost of the loan, as well as customer reviews of the lender. The interest charged is now deductible only if the loan is used to “buy, build or substantially improve” the home that is collateral for that loan. If the loan is used for those purposes, then a taxpayer can deduct interest on up to $750,000 of borrowing. This limit covers all real estate debt, including your primary mortgage(s).

The loan is then disbursed to the borrower as a lump sum, and the borrower must pay interest on the entire balance of the loan. And, because the loan is secured by the borrower’s home, the lender can foreclose if the borrower fails to make on-time payments. A home equity loan can be a better choice financially than a HELOC for those who know exactly how much equity they need to pull out and want the security of a fixed interest rate. Borrowers should take out home equity loans with caution when consolidating debt or financing home repairs.

What Is an Interest-Only HELOC? (2024 Guide) - MarketWatch

What Is an Interest-Only HELOC? (2024 Guide).

Posted: Fri, 19 Apr 2024 07:00:00 GMT [source]

A credit card is a line of credit that, unlike a HELOC, is not secured by your home or other property. This makes credit cards a good option if you don’t have enough equity in your home to qualify for a HELOC or can’t get a personal loan quickly enough. However, because credit cards are a form of unsecured debt, they typically come with a much higher interest rate and—depending on your credit—may not offer the spending power you need. Personal loans can be secured or unsecured, which makes them a great option for homeowners who don’t have much equity in their home or for borrowers who don’t want to pledge any collateral. A home equity loan is a fixed-rate, lump sum loan that is secured by the borrower’s equity in their home.

Generally, lenders require that homeowners have at least 20 percent equity before they can obtain a home equity loan product. Take your outstanding mortgage balance and divide it by your home’s appraised value to get a percentage for your LTV ratio. The rates featured here allow you to compare home equity lenders and see national averages so that you can make the best, most informed decision. When you shop for a home equity loan, find out the annual percentage rate (APR).

No comments:

Post a Comment